Is Venezuela Back? We Went to Caracas to Find Out

Notes from a week on the ground in Caracas.

For a very long time, Venezuela was uninvestable in the most practical sense of the word: sanctions, sovereign default, capital controls, regulatory opacity and a political situation that made institutional investors unwilling to even look. We were no exception. From 2019 to 2025, across the entire investment periods of our Funds I and II, we tracked a total of 6 Venezuelan startup opportunities and honestly, we never dug very deep into any of them.

And then, in 2026, something changed: on January 3rd, the US removed Nicolás Maduro from power, and the political landscape of the country started to shift, opening a door that had been closed for years. Our dealflow followed. By May, we had already received more than 30 Venezuelan opportunities.

The specific trigger for our deeper engagement was a founder introduction: Rodrigo Tognini, the founder of Conta Simples, one of our portfolio companies, introduced us to Enrique Rivas, CEO & Co-Founder of Fina, an SMB ERP growing unusually fast in Venezuela, and that conversation revealed something deeper than expected. Venezuela lacks basic financial infrastructure that was solved more than a decade ago in Brazil and other more developed economies. The problem goes well beyond the absence of venture capital. Payment rails, credit infrastructure, merchant software, recurring billing, and digital fiscal invoicing, the things that make a modern digital economy work, haven’t been built yet.

And yet, that gap hasn’t stopped companies from growing. Venezuelan startups are using creativity and extreme capital efficiency to find profitable growth paths in conditions that would have killed most companies elsewhere. That curiosity got us to commit time trying to better understand if a “Venezuelan Opportunity” exists. We met many founders, mapped the ecosystem and started a fascinating deep dive in order to size such opportunity.

Ultimately, this got us on a plane, and we spent a week in Caracas for Venezuela Tech Week, the country’s tech entrepreneurship conference. While we were there, Venezuela formally began renegotiating one of the largest unresolved sovereign debt loads in the world, estimated at $150-170B, with the country and PDVSA (Venezuela’s state oil company) in default since 20171. This has very practical implications: sovereign default blocks startups from international bank partnerships, access to credit, international settlement, digitally compliant payment rails, and prevents access to venture capital and exit opportunities. Debt restructuring is the precondition for those operational channels to reopen.

We are here to share what we learned and the opportunities we found.

TL;DR: Post-January 3rd, Venezuela is being reconstructed unevenly, politically, and with no clear rulebook, but the optimism and momentum on the ground are real. Great minds are returning to the country, companies are growing at rates that are hard to find anywhere else in the region, and if the regulatory and institutional framework catches up with what founders are already building, many significant opportunities will arise.

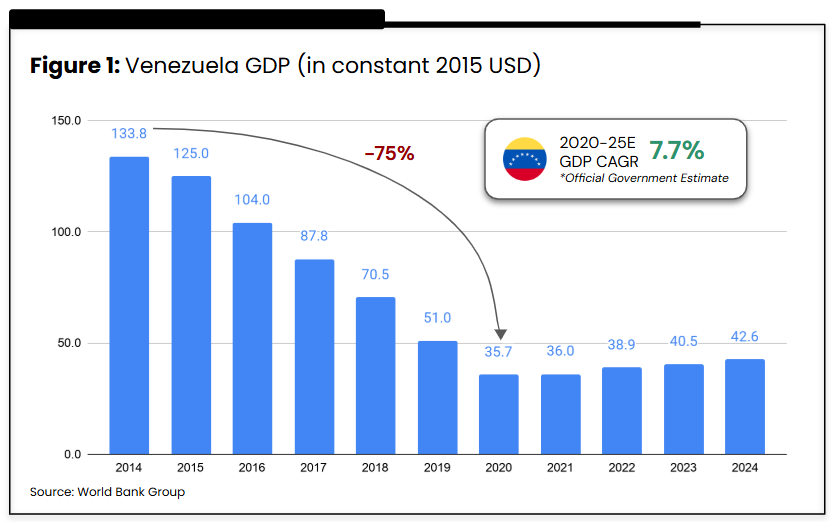

A $100B economy sitting on $372B of potential

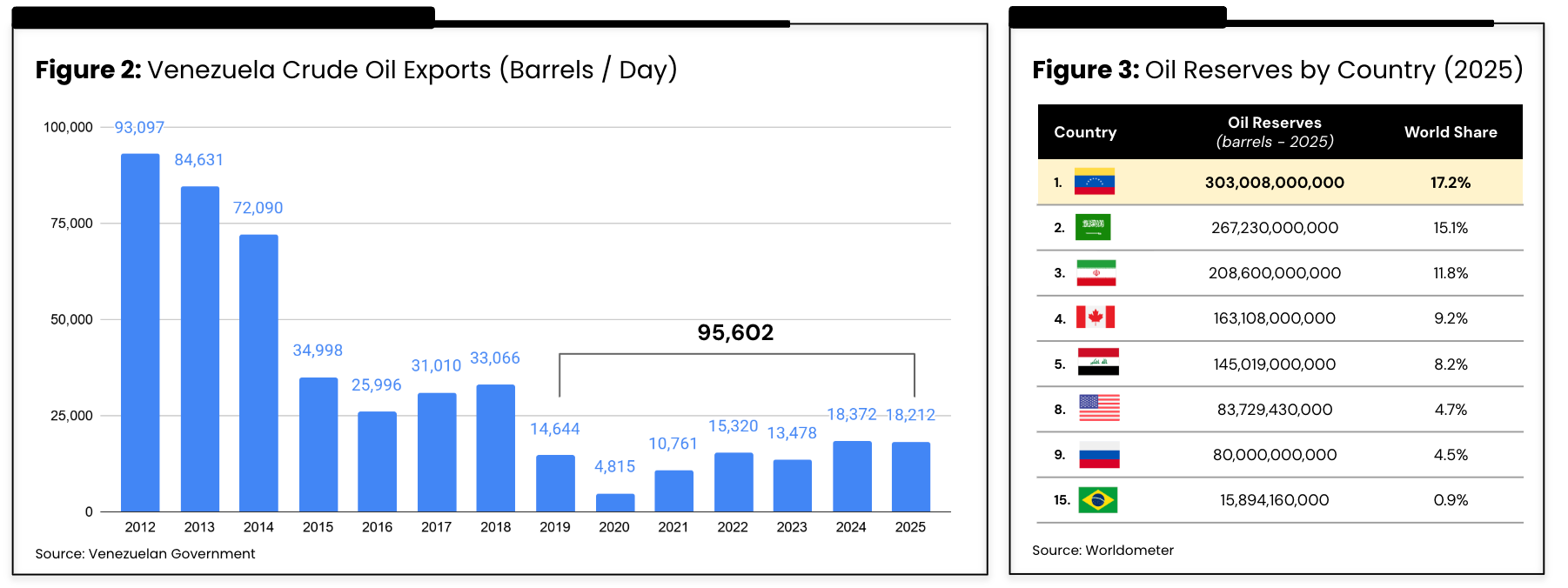

Official government data shows 5 consecutive years of real GDP growth. These figures come off a catastrophic base, since the economy collapsed from roughly $372B in 2012 to around $100B today, with oil exports reducing by 95% from its peak.

Venezuela holds the world’s largest proven oil reserves at over 300B barrels, and production has collapsed from over 3M barrels per day in the late 1990s to ~1M today.

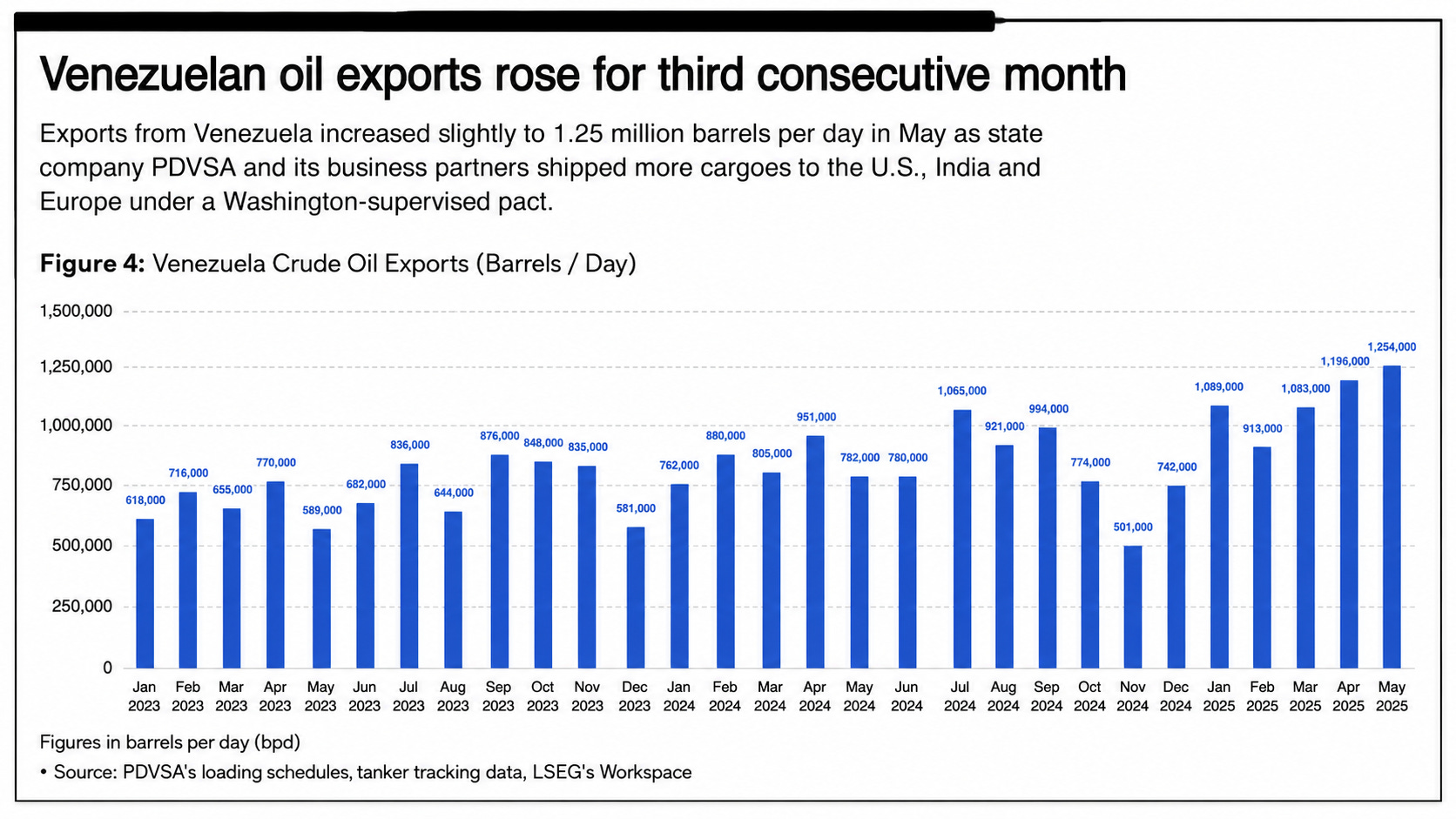

The installed infrastructure is enough to ramp up a good share of past production, and this ramp-up is already underway: oil exports rose to 1.25M barrels per day in May-26, a third consecutive monthly increase and 61% above the same month a year earlier, as Washington eased sanctions and foreign companies returned to the country. The oil ministry has forecast output of 1.37M bpd by year-end, a level not seen since US energy sanctions were first imposed in 20192. Reaching 2M barrels per day would require $8-9B per year in investments and could take until the early 2030s. A full return to historical production levels would demand even more, with estimates ranging from $53B-110B over 10-15 years3.

Beyond resources, the country has meaningful internet penetration (around 60%, the same level Brazil was a decade ago), and most surprisingly, a high banking penetration: in a session at the event, Calixto Ortega (the former head of Venezuela’s central bank and current economy VP) cited a banking penetration above 95% for Venezuelans over 18, a level that’s in line with Brazil and US penetration.

Venezuela is a financially distorted country, and the population moves constantly between bolivars (official currency), dollars, cash, Pago Movil (Venezuela’s instant payment system), informal FX, remittances, and crypto/stablecoin-based workarounds. A normal consumer or merchant in Caracas may understand liquidity management more viscerally than a much wealthier consumer in a cleaner economy, because the cost of getting it wrong is immediate, simply because, by holding Bolivars, they are losing 1% of their value daily, thus, any capital preservation effort requires converting your money to dollars fast, and accepting high spreads (3-7%). FX friction actually intensified financial behavior, forcing people to become more sophisticated about managing money across multiple currencies and instruments.

That distortion has also made the population crypto-native by necessity. Stablecoins, Binance Pay, and other crypto workarounds are embedded in daily commerce, for instance, Venezuela’s 2025 crypto transaction volume reached $44.6B4. People adopted crypto because the traditional financial system couldn’t serve their needs, and that adoption now represents a genuine advantage for fintech companies building in the country.

On the regulatory side, the environment remains a serious obstacle, but Venezuela appears to be entering a phase of selective, state-managed modernization. We spoke with several fintech startups in the region, all working towards obtaining their licenses to operate in the fintech space, many reported significant progress since Jan 3rd. One clear example, although still early, is that the Telco regulator just announced the approval of 15 new telecom operators in 20265, a signal that Venezuela’s regulatory gates may be starting to reopen for business. That single decision enabled an investment commitment of $500M by Telefonica6 to invest in the region’s digital infrastructure.

For fintech, licensing frameworks are still opaque, legal certainty is still unclear, and companies operating in good faith still find themselves in gray areas because the rules themselves are unclear or incomplete. SUDEBAN (banking regulator), SUNACRIP (digital assets regulator), FX policy, bank connectivity regulations, and compliance requirements all need significant improvement before institutional capital can deploy at scale. The government is starting to listen and engage with private-sector input, but the gap between openness and clarity is still wide.

Our call here is that as this modernization process continues to move forward, it will create asymmetric opportunities for companies that provide the infrastructure the country needs. It’s unclear how long it will take until Venezuela becomes a “normal” open market, but right now the country appears willing to approve new operators, renew licenses, and modify regulations in pursuit of rebuilding itself.

Credible currency: A necessity for the rebuild

The currency sits underneath many of the investment risks and opportunities in the country. Full dollarization is a problem for any economy: it means surrendering monetary policy, losing the ability to manage credit cycles and depending entirely on external dollar inflows. Venezuela needs a functioning domestic currency, which means the bolivar needs a credible revamp, something structurally similar to what Brazil did with the Plano Real in 1994.

Hyperinflation creates a self-reinforcing cycle in which people expect the bolivar to lose value, spend it as fast as possible, and hoard dollars, and that velocity of spending reinforces the very inflation they’re trying to escape. Breaking that cycle requires institutional credibility, fiscal discipline and a monetary anchor that people trust. Venezuela is still far from having those conditions in place.

One useful mental model we absorbed is that tracking the gap between the bolivar/USDC rates on crypto exchanges and the official exchange rate is a good proxy of the country’s stability (or journey towards it). According to several people we spoke to, a year ago, that gap was around 80-90%, and it has since narrowed to roughly 30-40%7. This gap effectively measures how much the market trusts the official rate, and by extension, how much it trusts the institutions behind it. Closing that gap further is a condition for the kind of macro normalization that would unlock the next wave of investment.

Capital scarcity breeds a specific kind of company

The absence of institutional capital for the last decade fundamentally shaped the Venezuelan startup ecosystem, and the companies that survived developed a very specific profile.

Most global platforms and US incumbents stayed out of the country due to sanctions, compliance risk, and FX complexity, and local companies filled the vacuum with limited competition but also without access to capital. They hired strong local talent at relatively low costs, built lean teams deeply familiar with the operating conditions and grew profitably by design, but also fast. Multiple startups are in the $1-10M revenue range, doubling or tripling year over year, a few with little (oftentimes less than $100K) outside capital and most with zero investments. This lack of venture capital forced a discipline that is unusual in any developed market. They had to sell, collect, retain, operate, and survive without the luxury of subsidized growth, which created an extremely resilient cohort of entrepreneurs.

Capital scarcity is brutal and kills most companies. But the ones that survive often look unusually efficient when capital finally returns.

In any other market, these numbers8 would already have attracted significant institutional capital, but in Venezuela, most of these companies built this scale nearly alone.

This looks familiar

If you’ve followed Latin American venture capital for the last 15 years, you’ve seen this pattern before. What is happening in Venezuela today resembles what happened in Brazil during the first wave of venture capital between 2010-15, when a set of local companies emerged to fill category gaps that global platforms either couldn’t or wouldn’t address.

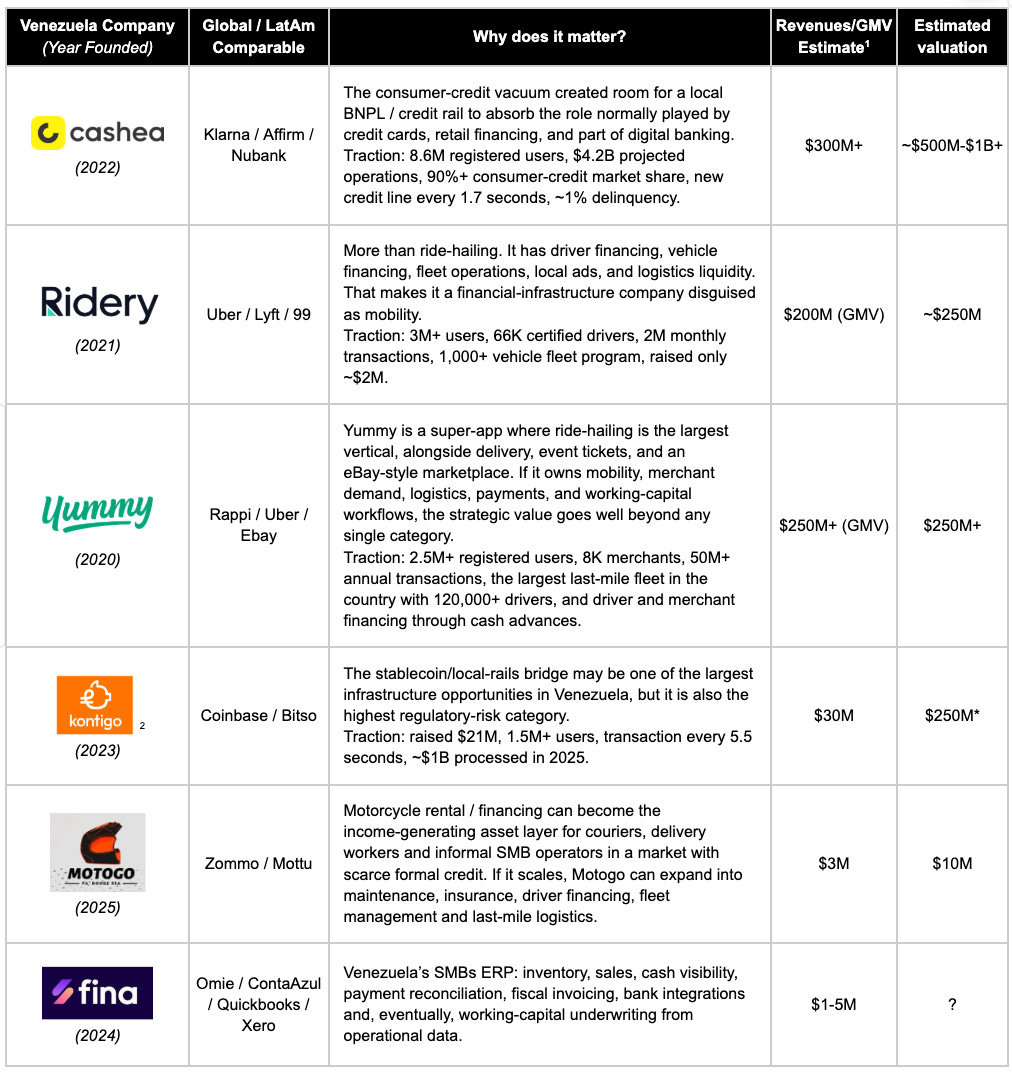

Brazil’s first tech unicorn was 99, a ride-hailing company acquired by Didi for $1B in 2018, and Ridery is a clear Venezuelan parallel. iFood became Brazil’s dominant food delivery platform, currently valued at $5.4B with near-monopoly market share. Yummy is building a multi-vertical super-app in Venezuela spanning ride-hailing, delivery, and marketplace, and has already moved into fintech with driver and merchant financing. Nubank redefined consumer financial services in Brazil and is now a $60B+ public company with over 110M customers, and Cashea is the closest parallel as a consumer credit platform that has reached massive scale. Omie and ContaAzul pioneered cloud-based SMB software in Brazil. In Venezuela, Fina is embarking on a similar trajectory, and although early, it seems to be taking the right steps towards building the operating system for small merchants in a market where most businesses still run on pen and paper.

As we mentioned in our “Man From the Future“ letter, sometimes, when you’ve watched a market structure mature in one geography, going to another geography where the same transformation hasn’t happened yet is like traveling to the past with insider information. Each country has its unique dynamics, but the pattern recognition shows us that there is a positive prognosis for the region, similar to what started for startups in Brazil around 2010.

Achieving fast growth with no funding is the strongest possible signal of product-market fit. When a company keeps doubling revenues without a dollar of venture, the demand is real and the unit economics have to work. That is happening for many startups in Venezuela right now.

The timing also helps. AI has fundamentally changed how much a small team can build. A five-person engineering team in a garage in Caracas today is also using Claude Code to ship at the speed that would have required 50 people a decade ago. Venezuela lost a massive share of its skilled workforce in the diaspora, and that would be a hard constraint on how fast an ecosystem can grow, but AI changes the math. The talent that stays becomes dramatically more productive, founders are finding creative solutions and leapfrogging infrastructure gaps that would have taken years to close manually. With AI, the ecosystem can reach critical mass without waiting for the talent to physically return and, for instance, this is a country with a population 5 years younger than Brazil’s9.

Brazil’s first venture wave happened at a time when building software was expensive and labor-intensive, Venezuela’s is happening at a time when it has never been cheaper or faster to build.

Another historical pattern is that the first wave of a nascent tech ecosystem is almost always consumer-facing. B2C companies reach scale first because they address the most immediate and visible needs. If the pattern holds, a B2B wave will follow, and the infrastructure layer of payments, compliance, merchant tools, credit scoring, and treasury management is where the next set of opportunities will emerge.

Every startup is a credit business

Understanding why every Venezuelan startup eventually gravitates toward financial services requires understanding what the financial system actually looks like on the ground.

Venezuelans already live inside digital and semi-digital money movements every day. The fintech opportunity is entirely about infrastructure: the tools, rails, and platforms to make it work properly.

Pago Movil gives Venezuela something that looks, from a distance, like real-time payments, but the architecture is far from what Brazil built with Pix. The user and merchant experiences are clunky and primitive by modern standards10. Fee friction on both the sender and merchant side also remains a structural weakness, and since credit cards account for less than 1% of transactions in the country, the entire consumer and merchant economy runs on a patchwork of cash, bank transfers, Pago Movil and crypto.

Think about what a Venezuelan merchant needs to know every day: what she sold, in which currency, whether the payment actually cleared, whether she can restock tomorrow, whether the bolivars she holds will lose value before she pays the supplier, whether her invoice is compliant, and if anyone will lend to her based on her track record. All of those questions map to infrastructure that exists in other countries and is absent or broken in Venezuela.

The consequence is that almost every valuable startup in Venezuela eventually gets pulled toward credit and financial services. In more developed markets, categories stay cleaner for longer, with B2B software remaining B2B software, mobility remaining mobility, and delivery remaining delivery. In Venezuela, the categories collapse into each other. Ridery can expand into driver financing, vehicle financing, insurance, fleet credit, and logistics liquidity. Yummy already offers driver and merchant financing through cash advances, and can expand further into courier financing, wallets, ads, and working capital. Fina’s real strategic value lies in the operational data it collects, including sales frequency, inventory turnover, and payment patterns, which become the raw material for credit scoring and working capital distribution.

January 3rd changed everything. Clarity still hasn’t followed.

January 3rd changed everything about how the world looks at Venezuela, and everyone we spoke with during the trip acknowledged it. In conversations with venture investors, founders, Ridery and Yummy drivers, hotel staff and random people on the street, we heard a consistent view: virtually everyone supported what happened, and there is a genuine sense that the country has turned a corner. People believe elections will happen eventually (MCM is winning our street polls by a very far margin), but our overall take is that elections are not what people are focused on right now.

The priorities we heard were: political stabilization, people want to know that the situation will hold and that the opening is durable; and fixing the basic things that have been inaccessible or broken for years, from infrastructure to public services to economic normalcy. The sense is that once those foundations are in place, a more open political process can follow. What brings them some comfort is that the international community appears engaged and attentive to how things unfold.

One telling anecdote: we were on the ground when Trump posted about Venezuela becoming the 51st U.S. state, and we asked Adolfo, our Ridery driver, whether he had seen the news. Surprisingly, he just waved it off. “Mi pana, aquí hay vainas más importantes que resolver [there are more important things to deal with]”. “People need their money to be worth something again. We need to know what the bolívar is worth today, and what it will be worth tomorrow. What matters now is whether the U.S. is buying Venezuelan oil and they just bought something like $600 million of it. The 51st state thing? Eso es ruido [that’s just noise]. I do think there will be elections by the end of the year, and I think María Corina is coming back. But for most people, esa no es la prioridad ahorita.”

We had the opportunity to meet senior economic officials, regulators, and government-linked entities to make the government’s posture visible and the engagement felt somewhat genuine. In a public session with foreign investors, Calixto Ortega laid out the current regulatory framework: Venezuela is reviewing its approach across banking, financing, real estate, hydrocarbons, mining, and other areas, and the fintech framework is open to input and potential amendments. When asked about SUDEBAN, SUNACRIP, and the fintech roadmap, the answer was closer to “we are revising everything” than “the rules are solved.” That’s constructive, and it represents a shift from a recent past in which everything that touched fintech/crypto regulation and licenses happened over closed doors (and thus was immersed in corruption11), but it is still far from the kind of clarity we’d like to see.

The government’s priority is to protect and relaunch the bolivar for domestic use while remaining open to tools that help Venezuelan entities interact with the international financial system. The founders who understand that framing and build compliant infrastructure that helps reconnect Venezuela to international finance will likely find more regulatory tailwind than those who position around replacing the bolivar.

Institutional clarity needs to improve significantly before the country can absorb serious capital at scale.

Company Spotlight: Fina Partner

Fina makes the thesis concrete because it embodies the full arc from operating pain to financial infrastructure. Three of the founders previously built Caracas Ron, a 24/7 liquor and food delivery business during COVID, and when lockdowns ended and demand declined, they struggled with inventory visibility, cash-flow management and working-capital constraints. Those are the same problems that every small merchant in Venezuela faces daily, and that experience directly surfaced the need for simple, affordable, localized operating software.

Fina’s typical customer is a micro or small business, usually owner-operated, with 2-10 employees, monthly revenue of roughly $1-5K, heavy reliance on Excel or notebooks before adopting software, and little or no access to formal credit. The product today covers daily operations including sales, inventory, basic financial control, and workflow visibility. The company has roughly 4,200 active customers, crossed $1.5M in ARR in a year after launch, and has a CAC payback below 2 months, growing at a very fast pace.

Their roadmap follows the financial-gravity pattern: fiscal invoicing, automated Pago Movil verification, real-time cash visibility, integrations with the four largest banks, POS integration, and credit. In its initial credit pilot with a Venezuelan bank, Fina reported zero delinquency, with customers paying their first installment an average of two days early, 10% prepaying the second, and not a single phone call required to collect. In a credit-starved market, the operating system of the merchant can become an underwriting system.

The risks are clear too. The customer base has limited pricing power, churn is front-loaded in the first three months due to incomplete activation and payment friction as there is no local Stripe yet, or an easy alternative recurring payments infrastructure. It’s all being built right now. The same infrastructure gaps that create the opportunity also make the company harder to scale. The company recently raised a seed round with local and foreign investors and is now in a strong position to accelerate growth even further.

At Fina’s offices we saw a high energy, great culture environment. We saw founders with the resilience required to tackle the challenges that their country presents. We’re confident that they will be able to devise clever solutions around the country’s challenges, and by being the first mover, that resilience puts them in a very interesting spot.

Sanctions accidentally built a moat

One assumption worth questioning is that if Venezuela opens, global platforms return and win. That may eventually happen in some categories, but it deserves skepticism. Venezuela never received the default global tech stack, and local companies were forced to build their own alternatives over years, oftentimes inventing completely new categories.

Will Visa/MasterCard eventually take over Cashea’s business? It’s hard to predict, but it doesn’t seem likely to us. Cashea became embedded in the company’s consumer culture and habits.

Will Uber eventually be a threat to Ridery/Yummy? More than just a mobility app, the company rents cars, gives credit to drivers, sells local ads and has a sophisticated business model that goes beyond what the surface shows.

These companies learned bank integrations, credit discipline, informal FX, local compliance and customer education in the field, over years of operating while everyone else was absent. Also, the average Venezuelan consumer is working on an older-generation Android device, connectivity is often limited to 3G speeds and apps need to be built from the ground up to perform under those constraints. A product designed for the latest iPhone on a fast LTE connection will struggle in that environment. The companies that grew in Venezuela learned to build lightweight applications that work on the hardware that people actually have, which is difficult to retrofit back.

Global platforms may eventually come back, but they will not come back to an empty field, and even when they come, it might make more sense to acquire and partner up than to try to tackle a complex market by themselves.

TAM can be a concern, but this is also a winner-take-most market

TAM is the obvious investor objection in Venezuela: the market is smaller, poorer, and more macro-fragile than Brazil, Mexico or Colombia. But that framing can miss the more important point: in markets where core infrastructure is broken or underbuilt, category leaders can capture an unusually large share of spend very quickly. Right now, there are at least 4 Venezuelan startups that have reportedly scaled to more than $100M in GMV / annual revenue within 3-5 years, implying that the country can still produce outcomes with venture-style return potential when a company owns a high-frequency, trust-critical use case.

Cashea is the clearest example: according to our sources, the company crossed $350M in ARR on just $2M of early funding, only recently raising a round close to $80M that puts it on a path to unicorn status. That matters because in Venezuela, a startup doesn’t seem to need a perfectly clean macro backdrop, since they have never seen one before. What they need is to become the trusted operating layer in a market where customers are desperate for reliability, and the first company to earn that trust dominates. And the market ceiling is higher than the headlines suggest, since in the good scenario where the country’s GDP returns to historical levels, it could grow 3x over the next 5 years.

Optimism informed by difficulty

The Venezuelan founder diaspora is starting to reconnect, and that reconnection works as a graph of capital, mentorship and distribution. We heard about founders and operators who spent years at Rappi, Nubank, or Mercado Libre, grew a Series B in Bogotá or Miami, or studied at top-tier universities, and are now starting to reconnect and build in a greenfield market. Companies like Slash, a Venezuelan-founded fintech building global payment infrastructure, prove that Venezuelan talent can build at global scale, and that same talent, credibility, and capital is starting to flow back into Caracas. These founders can skip a learning curve that Brazil’s first generation had to live through.

The infrastructure gaps are enormous and the addressable market is large, however the risk is also huge, since regulation is unclear, political transition is uncertain, the institutional credibility is still being rebuilt, the bolivar needs a solution and international access remains constrained.

But what stands alongside those risks is something hard to find elsewhere: companies growing at rates and capital efficiency levels that are almost unmatched in any other market we cover. The companies described in this piece have proven product-market fit under conditions far harder than what most startups face, and that kind of validation carries weight.

Easy markets don’t leave this much infrastructure unbuilt. Venezuela is being rebuilt. For investors willing to engage with the complexity, the asymmetry exists.

We are committed to continue spending time understanding the country and the opportunities it might bring, and willing to help local founders, regulators, and other investors figure out how to develop this ecosystem in a way that is good for the country, good for its population and ultimately delivers strong returns for investors. We came back more optimistic than when we arrived.

If you’re a Venezuelan founder solving one of these problems, we’d love to hear from you.

Venezuela is moving, and so are we.

Thanks to all our Venezuelan friends that reviewed early copies of this article!

Victor Charles Yitzhak, Freddy Genatios, Enrique Rivas, Daniel Bolivar, Nicolas Passaro, Luis Pernia, Carlos Ramirez & Adolfo Pecchio

Venezuela Launches Effort to Ease Its $170 Billion Debt Load, Wall Street Journal

Venezuela’s oil exports rose to 1.25 million bpd in May, shipping data shows, Thomson Reuters

Current production at ~1M bpd per OPEC/CEIC data, April 2026) and PDVSA CEO Hector Obregon, Malay Mail, January 25, 2026. Near-term recovery to 1.2-1.4M bpd per J.P. Morgan Global Commodities Strategy, January 13, 2026, which projects 1.3-1.4M bpd within two years of political transition; U.S. Energy Information Administration, February 2026, which estimated return to pre-blockade levels of 1.1-1.2M bpd by mid-2026); and Rystad Energy, January 2026, which estimates 250-300K bpd increase possible for ~$14B over 2-3 years. Medium-term 2M bpd estimates per Rystad Energy, which projects an additional $41B investment needed to reach 2M bpd by the 2030s; and J.P. Morgan, which sees 2.5M bpd potential over the next decade. Full recovery cost estimates per Rystad Energy, $183B total over 15 years for 3M bpd; TotalEnergies CEO Patrick Pouyanne, $100B estimate, January 13, 2026; Council on Foreign Relations, $10-20B near-term and $100B over ten years; Capital Economics, $15-20B for 1.5M bpd, via CNBC, January 28, 2026; and Enverus, 1.5M bpd by 2035, via Bloomberg, January 14, 2026.

Venezuela’s $44.6B crypto transaction volume per Chainalysis, 2025 Latin America Crypto Adoption Index (July 2024-June 2025 period), which ranks Venezuela 18th globally in crypto adoption and 4th in Latin America. The figure was confirmed in Chainalysis’ 2026 Crypto Crime Report, which noted that Venezuelan nationals were early adopters of crypto as a hedge against hyperinflation and sustained banking instability.

Conatel habilita 15 nuevos operadores, renueva 14 y modifica atributo a 9 empresas, Telecomunicaciones 360

Using USDT/VES as the reference crypto dollar rate. On May 29, 2025, Binance P2P was reported at Bs. 136.00 per dollar-equivalent versus the BCV official rate of Bs. 96.53, implying a 40.9% premium. By October 2025, Crónica Uno reported Binance USDT at Bs. 310 versus the official dollar at Bs. 197.24, a 57.16% premium, and noted that some merchants were already protecting against a gap above 70%. In late December 2025, BeInCrypto reported that the gap between the BCV dollar and Binance USDT had reached 87%. By May 29, 2026, usdt.com.ve showed Binance P2P at Bs. 742.65 and BCV at Bs. 549.37, implying a 35.2% premium.

SaaSholic estimates informed from boots in the ground research with founders, key market players and investors. WSJ reported that Kontigo faced allegations of sanctions-sensitive Venezuela flows/government-adjacent activity, lost access to partners including JPMorgan/Stripe/Bridge, and had its Venezuelan crypto license expire in Jan. 2026; treat compliance, licensing, and government ties as core diligence risks.

Venezuela is demographically younger than Brazil. In 2024, Venezuela’s median age was 30.2 years, versus 35.4 years in Brazil, a gap of 5.2 years. Venezuela also had a larger share of children, with 25.53% of the population aged 0 to 14 versus 19.67% in Brazil, while its elderly share was lower, with 9.68% aged 65+ versus 11.05% in Brazil. Sources: GeoRank, World Bank Data.

PagoMóvil lack clean merchant reconciliation, standardized metadata, programmable payment initiation, recurring-payment primitives, dispute tooling, developer abstraction and predictable settlement.

Great article.

Captured the opportunity, challenges, and nuance of this market.

So much work to be done, so many problems to solve, so much investment needed.

What a read! Spot on. For years Venezuelan talent left because they had no choice, so seeing real intent to change at the top is huge. If that turns into actual regulation, it's a boom. Whoever's already on the ground planting seeds gets to find out first if the soil is fertile. Excited to follow this one.