SaaSpocalypse: We Have Met the Enemy and He is Us

A redacted version of our 4Q25 Letter from the GP

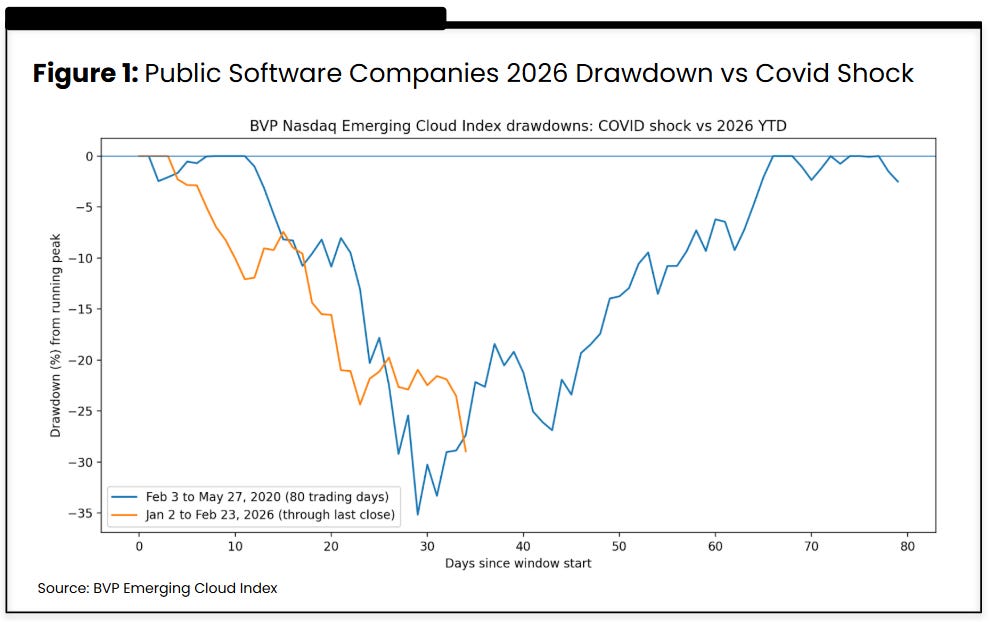

The day has come. Software is officially dead (again)! At least this is what the public markets seem to have decided. In the last twelve months, public SaaS is down an average of 32%1, and the drawdown has already surpassed the COVID selloff.

SaaS has, for two decades, been the holy grail of tech investing from Silicon Valley to Wall Street. The business model combines economics that let it compound over time: high growth, high margins, an asset-light structure with high switching costs and recurring revenues, leading to great retention that enabled tech companies to grow faster than other publicly traded industries.

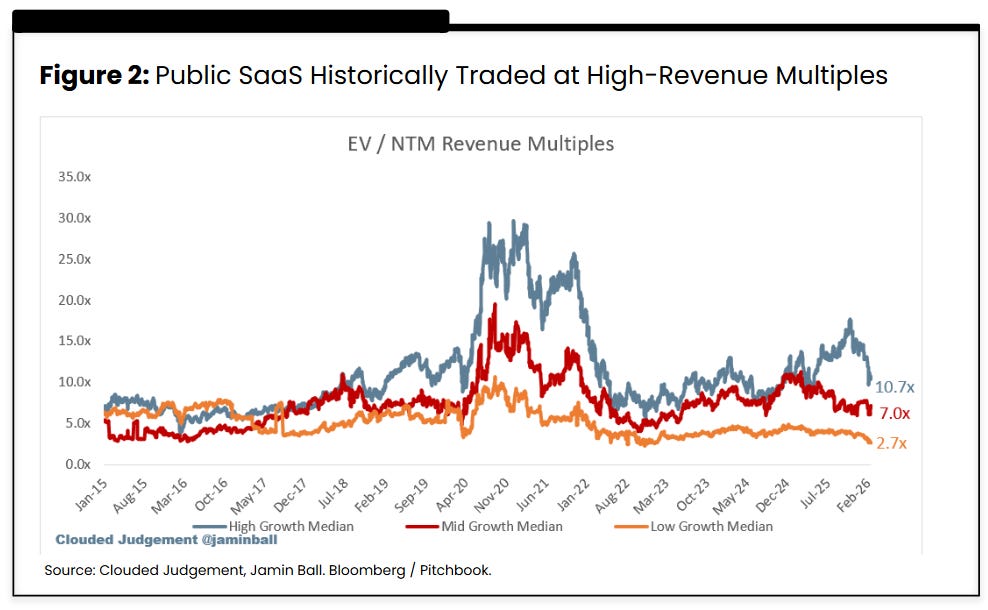

Cloud software has consistently grown 30% annually for 20 years, giving comfort and the benefit of the doubt for investors to “pay up” for a growth that would always arrive. High growth was rewarded in a world where growth in the real economy was harder to find and interest rates were 0. This led SaaS to trade at high revenue multiples (without needing to worry about profitability, yet), with the median SaaS trading from 5–10x ARR and top-quartile growth names at 20–30x.

However, it seems like AI is challenging every single one of the assumptions that made SaaS the hottest business model in town.

As seed investors not directly exposed to the public downturn, we believe the AI-driven reshuffle is good news. The largest names in software a decade from now will probably look very different from today, opening the doors for newcomers to build the next wave of winners.

Let’s break down what is driving the market pessimism.

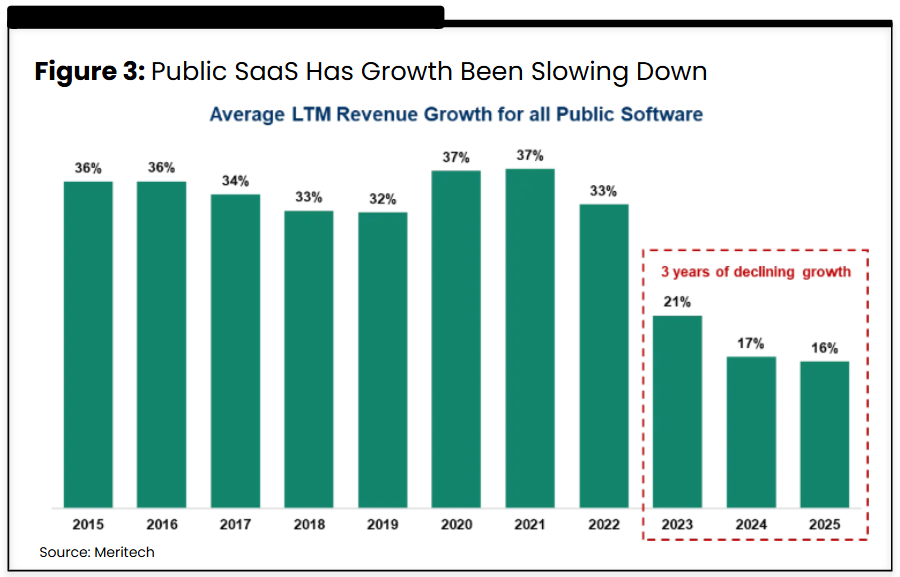

Public market growth is not what it used to be

Markets want high growth. However, growth rates for public SaaS have been declining for years. At the same time, AI is the new highest-growth opportunity available, and we have seen many AI companies beating record revenues in short periods of time, whether in the LLM space (Anthropic growing from $0 to $10B ARR in 3 years), the application layer (Cursor from $0 to $1B in 2 years), or infra (with NVIDIA’s revenue quadrupling to $130B since 2022).

Markets are searching for growth and public SaaS isn’t fully delivering it (which also helps explain why more dollars are flowing to private markets).

Many factors can explain this slowdown. SaaS has eaten the lion’s share of the on-premise software market, but it has now reached a stage where most large customers that need a CRM or an ERP at scale already have one (in developed markets, Latam still relies heavily on pen and paper). The growth fight is no longer SaaS versus on-prem, it is SaaS versus SaaS, be it horizontal or vertical, all competing for the same budgets and workflows.

This was already true before the AI era, but now, as the marginal cost to produce software is approaching zero, competition is becoming even harsher. There is now a new source of pressure from foundational model companies pushing into the application layer and vibe coding tools that make it easier for teams to build software internally.

SaaS has also historically been sold by seats, and as AI replaces parts of human work, seat growth naturally slows, removing one of the simplest engines of expansion for most businesses.

Markets are pricing in that these forces reduce marginal demand for traditional software, hurting perpetuity growth rates and justifying lower multiples.

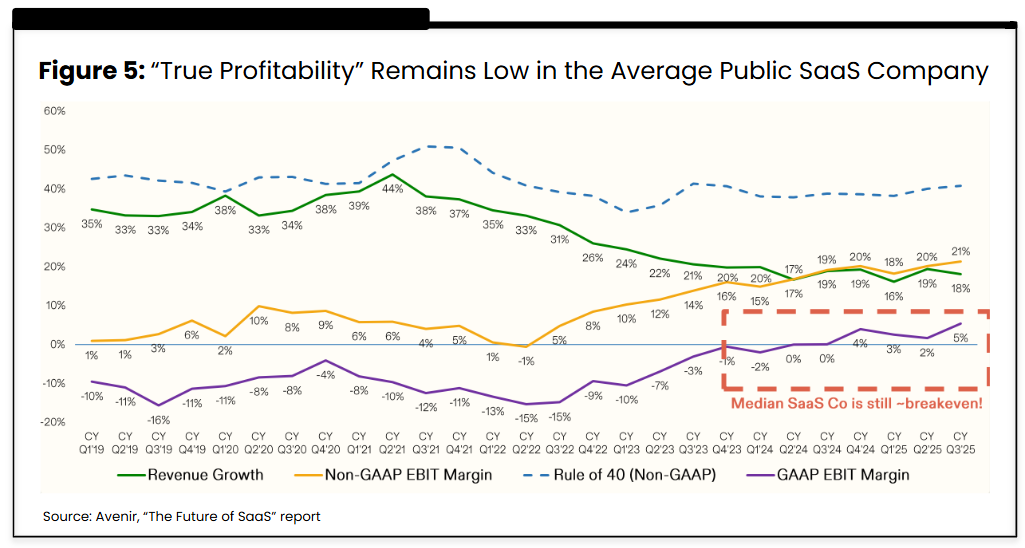

Real Profitability is Almost Nonexistent

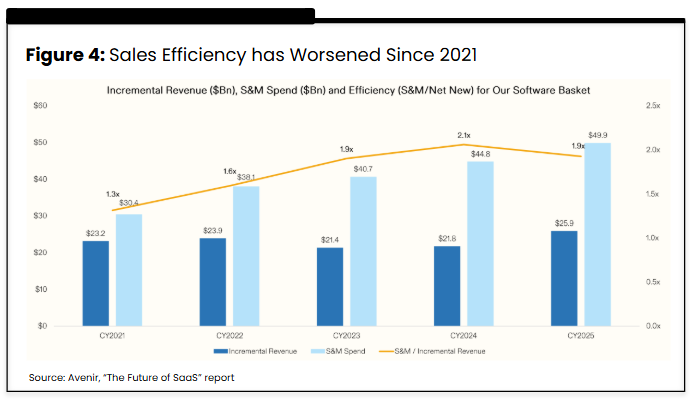

One of SaaS’s strengths was the near-zero marginal cost to serve, but gross margin masked a growing set of costs elsewhere. As markets matured, sustaining growth required meaningfully higher Sales & Marketing spend, more ads, larger go-to-market teams, which raised CAC and reduced sales efficiency. Attracting and retaining top talent also started requiring richer compensation packages, often delivered via Stock Based Compensation (SBC).

Financially, the incentives pointed in that direction. Even if sales efficiency deteriorated and a company had to spend, say, $2 in S&M to generate $1 of revenue, if that revenue was valued at 10x then it was still turning $2 of CAC into $10 of market cap, a 5x return. It was rational for companies to seek top line growth over profitability, as long as the market kept rewarding it.

After the ZIRP (Zero Interest Rate Policy) era, growth has slowed down and investors started to require a “get profitable” approach, but most legacy SaaS companies have still been unable to accelerate growth or profitability.

In the AI age, the growth outlook for these players is more challenging and serving customers is no longer free, since AI inference introduces a real cost to deliver value. If a company struggled to produce strong margins during the blue-ocean years, investors assume those margins will be even harder to reach in this new environment.

Switching Costs are Down

High retention was table stakes for great SaaS. Once a company installed a CRM or an ERP, switching was painful and risky. Even if a cheaper alternative existed, teams were already trained on the product, workflows were built around it and the software had become the single source of truth for the business.

Migration was not only expensive, it was a career risk. If you pushed a switch and it failed, you would get fired. This dynamic lets the best SaaS companies upsell their installed base with limited churn, with top players reaching roughly 120% net revenue retention.

Investors are challenging this moat in the AI age.

First, a surge of AI tools that execute workflows on top of existing systems of record is appearing, capturing value at the agent layer while using the underlying system primarily as storage. OpenAI’s Frontier2 release explicitly points in this direction, agents acting on top of users’ existing systems, rather than forcing a full rip-and-replace.

Second, AI agents may lower the practical switching costs by making migration less painful. If agents can move data from one system of record to another in a faster and cheaper way than in the pre-AI age, another part of the traditional retention moat weakens.

However, both dynamics only become real if incumbents keep APIs open enough for external agents to act on top of their platforms and if they fail to move fast enough to embed agents natively. Switching costs may fall, but only to the extent that systems of record allow themselves to be disintermediated.

Salesforce has been the prime example on both fronts. Agentforce, its AI agent platform, has already reached $540M in ARR, growing 330% Y/Y3. In May 2025, Salesforce limited Slack’s API, allowing only one call per minute and 15 messages per request, explicitly to limit third-party activity on top of their data4.

Incumbents will do what they can to build walls around the valuable data and distribution they already control.

So, is Software Dead?

What we have done so far is compile the most common bear arguments about the death of traditional SaaS. We don’t believe the market is getting everything right.

We understand that the combination of slower growth, lower profitability, and rising competition on public names naturally leads to a wider dispersion of outcomes, so the discount rate should go up and some level of correction is justifiable.

However, it’s crucial not to throw the baby out with the bathwater. As in every tech wave, AI will create winners and losers. The winners (and the market hasn’t decided who is who yet) will be the ones that can reaccelerate growth by embedding AI into their business or becoming truly profitable, earning their way back to top multiples. The losers will be disrupted and ultimately trade on FCF / earnings multiples, far below what an ARR multiple looks like.

George Soros’ reflexivity theory applies here. When SaaS stocks were up, the category benefited from a presumption of success, which reinforced more and more capital to be deployed. Now that many of these stocks have fallen, the presumption flips to failure. SaaS is not only down because it will perform badly, but investors start believing it will perform badly because it’s down.

Since the market punishes full categories faster than fundamentals change and the best companies often get repriced alongside the rest, this creates opportunities.

AI is also Software!

What the broader narrative gets wrong is mixing the negative impact on some mature public SaaS names with the death of software as a category.

Software is becoming more powerful than ever in the AI age, and many of the so-called AI winners that are “killing software” are, in reality, software companies using AI to deliver more value. That is true for all newly minted AI-native unicorns, such as Harvey, OpenEvidence, Sierra, Lovable, and Perplexity, and for the hottest Latam rounds too.

We believe this is one of the best moments in history to build and invest in software, and in the next sections we’ll pressure-test the loudest arguments claiming the opposite:

Companies won’t vibe-code their own SaaS

Applications won’t die because companies will rebuild them from scratch on Replit or Lovable. And it’s important to remember that Claude Code and Codex will also help enterprise vendors to ship faster!

SaaS includes the “software”, but also the “as-a-service” component. That service component is what keeps the product bug-free, secure and compliant 24/7, which is where vibe-coded software tends to lose to off-the-shelf products.

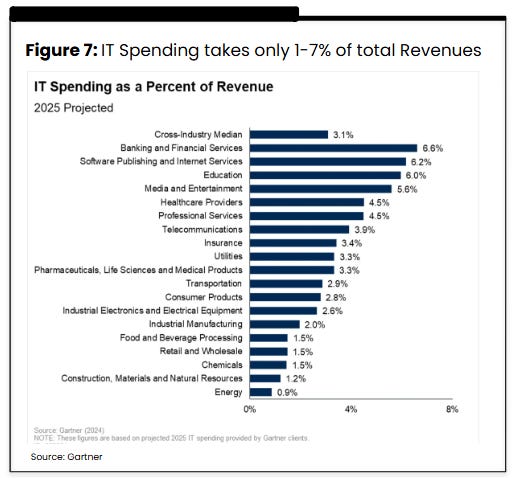

Additionally, IT spend is usually 5-10% of companies’ total budget. Why would a company focus scarce engineering resources to rebuild something that is currently working instead of trying to find new AI revenue lines that can drive real product improvement and growth? The math doesn’t add up.

Companies will still buy off-the-shelf software applications and the apps that can generate the most value, be it startups or incumbents, will keep winning.

Foundational Models won’t Replace (All) Apps

Another argument is that foundational models will have capabilities that are enough to replace entire applications. There have already been software applications totally disrupted by foundational models5, and LLM companies are increasingly going after verticals (earlier than we expected). OpenAI has launched Health, and Anthropic is going after Legal and Finance. For us, this is a more serious threat.

However, it seems unlikely that a generalist company will consistently ship the opinionated UI, workflow depth, and edge-case handling required across every vertical and geography, which is why applications still thrive.

Different foundational models are also better at different tasks. Gemini tends to excel at some tasks, while Claude and ChatGPT at others, which is why the best applications will often orchestrate multiple models instead of relying on just one.

We believe there are also ways to defend against this. Proprietary data in a vertical that general models cannot access can let you build a more capable, cheaper system for that specific task, and create differentiation even as the base models improve.

Seats are being reduced, Agentic work is growing, and fast…

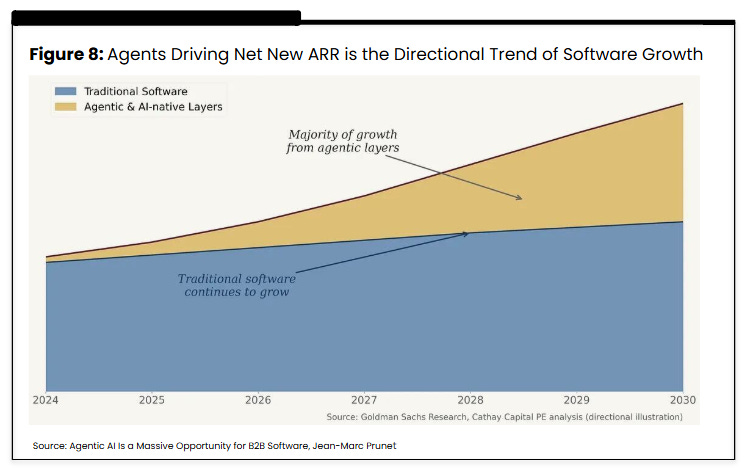

We agree that the seat-based pricing model is under pressure, and we have been calling this out for a while, like in our Superintelligent Software and The ARR Challenge essays. We are already seeing it in practice. Just last Thursday, Jack Dorsey’s fintech Block announced6 it is cutting 40% of its headcount as AI tools absorb more work. The stock jumped more than 20% in the next session. We expect other public SaaS companies to follow, driven by AI automation and the unwind of COVID-era overhiring, limiting net-new seat growth.

We do not think this means software stops growing. We think growth migrates to pricing models that are better aligned with value creation, be it usage-based, consumption-based, and in the best cases outcome-based. The chart below illustrates what this shift in the growth profile may look like: “traditional SaaS” trends toward residual growth, while the agentic layer drives most of the net new revenue.

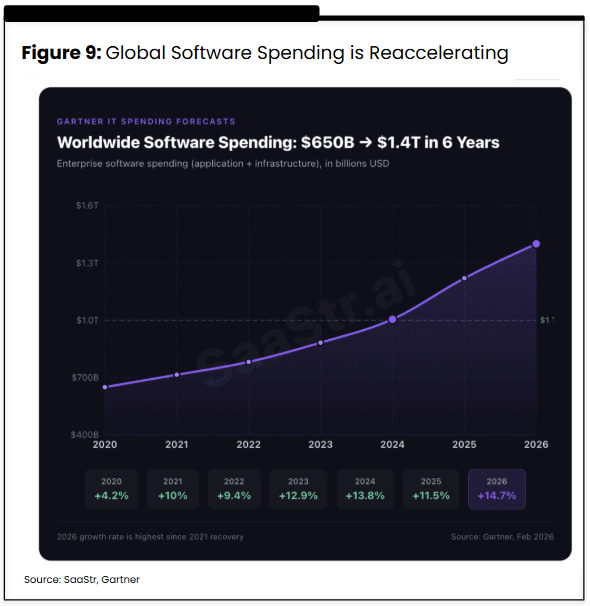

This shift has already started. 2026 is expected to be a year of not only growing, but accelerating software demand. As more budgets move from labor to software, the best players will capture outsized value and expand margins, while companies that rely only on seat-based expansion will feel the squeeze.

Startups have the right to win!

“The battle between every startup and incumbent comes down to whether the startup gets distribution before the incumbent gets innovation”, Alex Rampell7

This market reshuffle is the window for startups to rewrite categories. Startups can ship faster, take riskier product bets, and iterate continuously, while incumbents often have to navigate politics before doing anything bold.

We are happy to be on the innovators’ side of the table. This is the moment to rebuild legacy systems for the AI age and we are excited to back the teams redefining what software looks like next.

How to Win in the AI Era

We have been communicating since last year what we find valuable and continue to focus on the key moats software must have in the AI era, moats we believe will matter just as much for Latam seed as they will for the blue-chip public software globally.

In our view, enduring AI winners will share a common set of characteristics:

War-ready leadership team. Leaders who go into “founder mode” with the paranoia that what used to work won’t work anymore, rethinking how you generate value for clients and moving before the market forces you to.

Network effects, the ultimate moat. When usage improves the product and that improvement attracts more usage, the network advantage becomes hard to catch. In AI, where models and features commoditize, network effects can be the difference between a feature and a platform.

Product velocity and momentum. Shipping is faster and cheaper than ever. There is no reason to wait six months to release meaningful value. Momentum itself becomes a moat when the market is shifting weekly.

Touching money. Software that processes transactions, originates credit, or generates demand sits closer to value capture. It becomes harder to replace because it plugs directly into cash flow, not just workflow.

Proprietary data and vertical depth. Winners that leverage domain-specific data that other companies (even foundational models) do not have. They turn that data into outputs clients cannot get elsewhere and into products that help with the messy edge cases of a real industry.

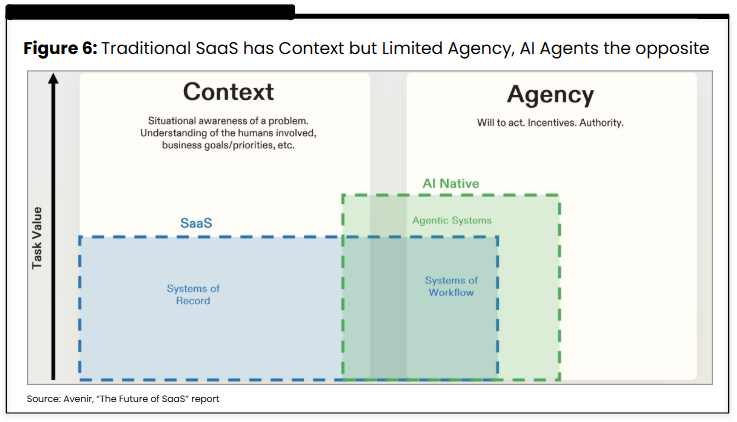

Outcome-based pricing through a system of action. Becoming a system of record is not enough. The long-term prize is evolving to become the system that executes work, closing the loop by having the context and execution. Aligning pricing with outcomes is what enables labor replacement and captures a fair share of the value created.

Memory moats, products that get better with usage. The best products learn from usage and context. When the software remembers how work gets done, switching becomes an operational nightmare.

Local moats. Regulatory compliance and local market structure can bring defensibility. In over-regulated or highly local industries, an off-the-shelf global product often cannot compete with a solution built for local realities.

API integration and agent readiness. The platform should integrate cleanly into the tools clients already use and be usable by agents, not just humans. Easy integration makes adoption faster, and it turns the product into infrastructure rather than a destination.

Low-friction, low-CAC distribution. More companies than ever are competing for attention and paid acquisition keeps getting more expensive. The winners build distribution that scales without linear spend, through virality, partnerships, or proprietary channels.

Multimodal, where the work happens. Work is moving across WhatsApp, voice, email, and existing systems, not into new dashboards. Products that meet users where they already operate will be adopted faster and stick longer.

We’re certain that what brought the winners of the cloud wave here will not bring them future success, which is why we are more excited than ever to be investing today and backing the future winners. The prize for the winners is greater than it has ever been!

As of 23-Feb-26, considering mean returns from the Meritech SaaS Index. YTD mean performance is -23%.

Launched on Feb-2026, Frontier is an enterprise offering for building, deploying, and managing AI agents that plug into a company’s existing systems of record, such as CRMs, ticketing tools, data warehouses, and internal apps data

Open APIs Are Over, Tomasz Tunguz

I agree with most of the analysis here, but there's something nobody wants to say out loud: the SaaS companies getting crushed right now were already bad.

I build SaaS. I see retention dynamics from the inside. And the uncomfortable truth is that a lot of these companies confused "high switching costs" with "good product." Customers didn't stay because they loved the software. They stayed because leaving was terrifying. Three-year lock-in contracts, deliberately painful onboarding, closed APIs. That's not a moat. That's a hostage situation.

What AI actually did was hand customers the escape tools. When migration gets cheap and fast, the only thing keeping people around is whether your product is worth paying for every single month. No safety net.

Now, the SaaS that never needed a contract to retain users, that keeps shipping features people actually asked for, that treats AI as a way to 10x value instead of something to defend against... that's not dying. It's growing faster than before.

This isn't a software apocalypse. It's a quality filter. And it took way too long to arrive.